The underwriter buy bond from issuer & sell to the public

Institutional investor are largest players

After selling, underwriter have nothing to do with the bond – another fiduciary agent handles day to day payment (usually bank as trustee for bonds)

Indenture

Also includes where the money to pay debt comes from

Also some condition to redeem bond in full before maturity date – “call”

Prospectus

Printed before sale, called “preliminary prospectus” / “red herring” / “official statement” (OS)

Who issue the bonds

Treasury / corporate / municipal

Some bond has high liquidity for secondary market, others don’t

Chap-2 Basics

Bond not traded on exchange, but OTC

Independent brokers

Big dealers: banks/pension fund etc.

Primary dealer – buy bond from Fed/Treasury and sell to public

Big size in bond wholesale market

US gov bond min lot $1M, common trade $100M

For individual investor, higher commission

Bid/ask spread – liquidity

Higher Liq lower spread

Dealer vs. Broker

Dealer have inventory, brokers don’t

Dealer put their own money at risk

E-platform

4 dominant: bond desk, municenter, knight bond point, trade web.

Terminology

Par – $1K

Discount vs. Premium

CUSIP – UID (nine digit number, equivalent to ticker)

CINS – international bonds’ CUSIP

Coupon – default – paid semiannually

Say 5.25% coupon means $26.25 interest income every half year.

Maturity – 15 means 2015. Usually maturity < 30 years.

Price: 97, means $970

Accured interest

Bond earns interest every day, when buying bond, sellers have accured interest which means higher actual price for buyer

Call risk – prepayment risk

Good for issuer of bond, bad for buyer

If bond purchased at premium, calling means directly losing money!

If bond rate higher than current interest

Conservatively assume it’ll be called

Evaluate based on yield-to-call instead of yield-to-maturity

Form of bond – certificate / registered / book entry

Basis point – 10bps is big diff for yield

Chap-3 Volatility

Two primary factors for price movement of bond

1. Interest rate risk

2. Credit risk

Interest rate risk / Market risk

Example: you buy treasury when yield=4%, now interest becomes 10%, you will sell at discount such that buyer’s yield is 10%. In this situation: sell at 30 cents on a dollar for treasury.

Ways to protect: shorter maturity bonds (< 7 year)

Maturity length related to interest rate volatility

The reason why shorter term bond are considered cash equivalents is because the price change little w.r.t. interest rate

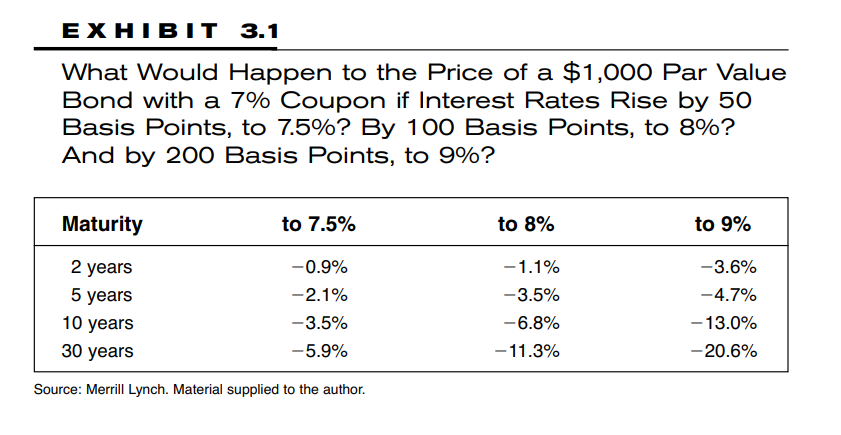

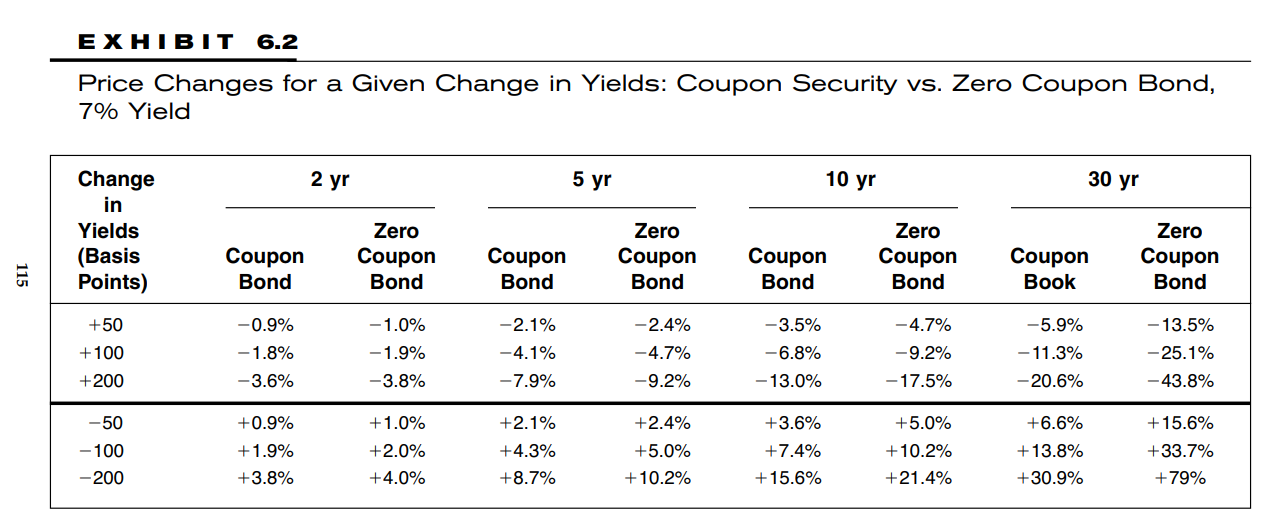

Rule of thumb: 1% increase in yield make 10% principle loss for 30-year bonds

How interest rate change in 50/100/200bps will change price for different maturity, assuming 7% interest currently

As bond approach maturity, their value approach par.

Price changes will be lower than this if it’s less than 6%.

The degree it’s affected by interest rate is increasing at a decreasing rate. (i.e. for 10-year bond vs. 30-year bond).

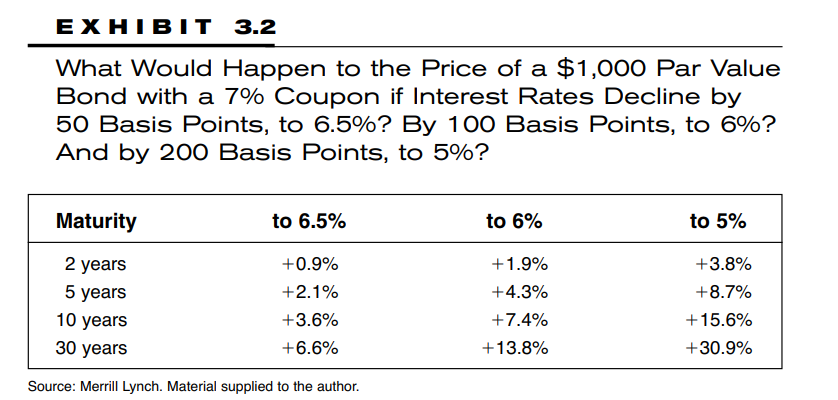

Convexity – second order Adj

Decrease interest rate has a bigger magnitude of price increase than the magnitude if interest rate increase.

Buy long term bond to bet interest rate will be lower – capital gain

Held to maturity – sell at par, regardless of interest rate path

不同利率下旧债换新债 – swap – no gain/loss but can generate tax loss!

Credit Risk

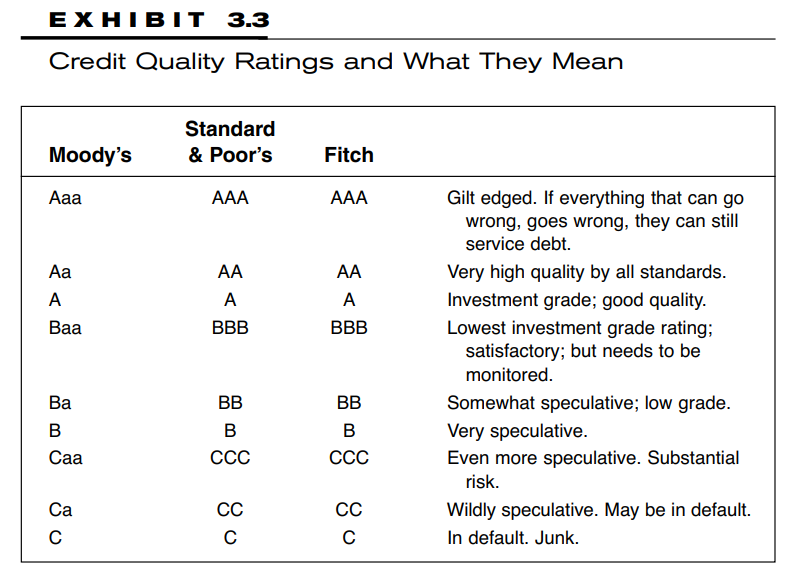

Credit rating – risk of default

Default measures both principal & interest

US gov considered zero default risk

How credit rating assessed?

Revenue over debt life vs. cost of debt service

Price change: upgrade price rise

Magnitude of price change from credit rating is less than interest rate (unless company truly likely to default)

Not every downgrade is equal

Below investment grade / drop more than one notch / series of downgrades in close succession is more important

Salvage value of defaulted bonds – can be purchased 10-30 cents on a dollar

Credit quality spreads, narrower when econ is good, wider when econ recession.

Maybe 10-20 bps between diff=1 notch for bonds maturity < 5 years.

2008 GCF – mortgage backed bond market

Credit rating AAA – suddenly collapsed

In municipal bond market – spread between AAA- & A-

Normally 50~70 bps (prior to GFC) suddenly becomes 300bps!!

Short history of interest rates

1950-1982 – principle declined by more than their interest for bond

1970s – coupon 4-6% principle declined 50% or more

Nominal return & real return

TIPS & I-bonds

Fed

Control Fed Fund Rate & Discount rate

Shortest: overnight rates

Fed Fund Rate: Fed’s interest for bank borrow overnight money to satisfy capital requirements

Discount rate: Between banks (similar to fed fund rate)

These directly affect short-term rates & 2-5 year bonds. But longer term may not be affected.

Purchase/sell treasury via Primary dealer to increase/decrease money supply.

Chap 4 – Basic bond math

Three sources of income

Simple interest + Capital Gain + Compound interest

Power of compound interest

7% interest rate w\o compounding 30 year is 2.1x par of interest. With compounding, it’s 6.8x par of interest.

Yield

Coupon yield – denom is par.

Current yield – coupon / purchase price.

Yield to maturity

Include interest-on-interest + capital gain

金融计算器

assume coupon income reinvested at YTM rate

assume hold bond till maturity

reinvestment risk – zero coupon bond no reinvestment risk

Longer maturity bond – less accurate YTM, because reinvestment is bigger portion of bonds’ return

Yield to Call

When multiple call dates

Yield to worst – lowest yield on all call dates

Same calc as YTM

Total return (a posterior)

Actual earning after you redeem/sell the bond

user for “marking to market” calcs

Duration

Gauge sensitivity to interest rate

Considers the timing of cashflows

Weighted average term-to-maturity of cashflow (def of duration)

Duration correlated to maturity length, but adjusted for size/timing of cashflows.

Lower coupon, longer duration.

Except zero-coupon bond, duration always < Time to maturity.

Duration can be used to calculate approximate interest rate volatility.

When interest rate goes up/down 100bps, price go by (approximately) duration of the bond.

Duration can also be calculated for a portfolio of bonds (weighted avg duration of all bonds in portfolio)

Duration works more accurately for smaller change of interest rate.

Convexity – duration的二阶修正

Chap-5 买之前需要知道的

Treasury

基石

Treasury notation

“Minus .01” means (-1/32 * 1%)

“99.29” means 99 + (29/32)

Yield curve

Change continuously thru-out the day

Steep: if long term & short term diff by more than 2%.

Flat: if long term & short term diff by < 1%

Reason behind yield curve

If expect inflation & rate hike – 涌入short term bonds (导致short term yield 下降)

If expect lower econ growth/降息, lock-in longer term bonds for high yields (long term yield下降).

策略 – Riding the yield curve

Buy a longer term bond and sell it in shorter term

Higher yield + price movement because maturity towards par

If interest rate increase, it will backfire (because you take a higher duration bond)

Yield curve – market consensus – predict econ

Additional ret for interest rate risk

2-7年可能比三十年收益率少30-50 bps 但interest rate risk少

Municipal bond往往更upward sloping

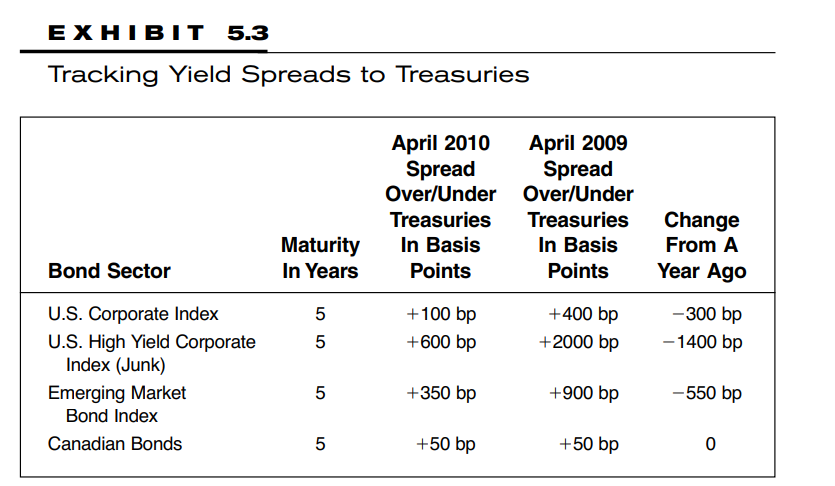

Spread table example:

Yield spreads & Benchmarks

Spread def – diff of yield between treasury and other bonds

When Econ bad – spread worsen

Junk bond price decrease & treasury price increase

Benchmark – Bond ETF

Chap 6 – Treasury, Saving bonds & Fed Agency Paper

Fed has either:

1. Treasury Bills / bonds or

2. Zero coupon bonds (zeros)

3. Saving bonds (EE&I)

4. Bonds from Fed Agencies

Treasury

Tolerance for interest rate risk

Flight to quality buying – 股票不好时把钱放进国债

issued periodically by Treasury & Sold thru auctions, most of which to “primary dealers”. In theory you can purchase treasury directly for $5-10MM

No state/local tax

T-bill 一年之内 – no coupon, discounted from par instead

Very short-term so interest rate risk can be ignored

T-notes (2-10 years)

Typically 50-150bps higher than T-bills

T-bonds (10-30 years)

Significant interest rate risk

TIPS (treasury inflation indexed securities)

Face value adjusted by CPI-U

Interest rate never changed but face value does

Interest rate is fixed per auction

High volatility – lower coupon – higher duration

Inflation Expectation Changes

Higher interest rate risk

Big drawback – taxed annually for phantom income

i.e. the capital gain from TIPS because of inflation

Comparing TIPS vs. T-bond etc.

Breakeven inflation rate

Zero coupon bonds (a.k.a. “strips”)

Tax: need to pay imputed interest (phantom interest) every year

Used to speculate

Municipal zero might be more tax-friendly

Warren Buffet buy 30-year zero for speculation

Series EE & Series I

Deferred tax on all interest until redeemed

Education Tax Exclusion

Series EE: accural bonds, no interest until redeem

Series I: 收益公式较复杂

Federal Agency

Credit quality slightly worse than treasury

usually 50-150 bps

Example: Fannie Mae, Ginnie Mae, Freddie Mac

Under conservatorship of Gov.

FHLBs/TVA

Tennesse Valley – 美国power system (国企)

CDs

Insured CDs – sold by some brokerage

Offers Buyback (floating principal) options for early liquidation